The rising balances of traditional private student loans are a major problem. Signing up for a traditional loan without knowing exactly how much you could be paying back or how you’ll be able to handle your monthly payments could be difficult.

One solution that has been gaining traction among online bootcamps and colleges alike are Income Share Agreements. (ISAs).

An ISA is an agreement where, in exchange for tuition, after graduation and as long as you’re earning an agreed-upon income, you pay a percentage of your income back to the college (or funder). Besides the absence of growing interest and generally, no upfront payments, a significant benefit of ISAs is the fact that there are certain instances when your payments are paused or deferred.

With traditional private student loans, you have a principal, the borrowed amount, and an interest rate. You pay back the amount of the principal plus any interest you accrue while paying it back.

ISAs keep students from paying for educational experiences that don’t create value for them in the labor market, aligning the risks and rewards of education and creating better outcomes.

Are you considering signing an Income Share Agreement? Here’s what you need to look out for before you sign your agreement to make sure your payments are manageable.

What are the ways to finish my ISA?

By far the biggest differentiating factor between ISAs and traditional student loans, other than the built-in benefits, is the way they’re satisfied. With an ISA contract, there are three distinct ways you can finish your ISA:

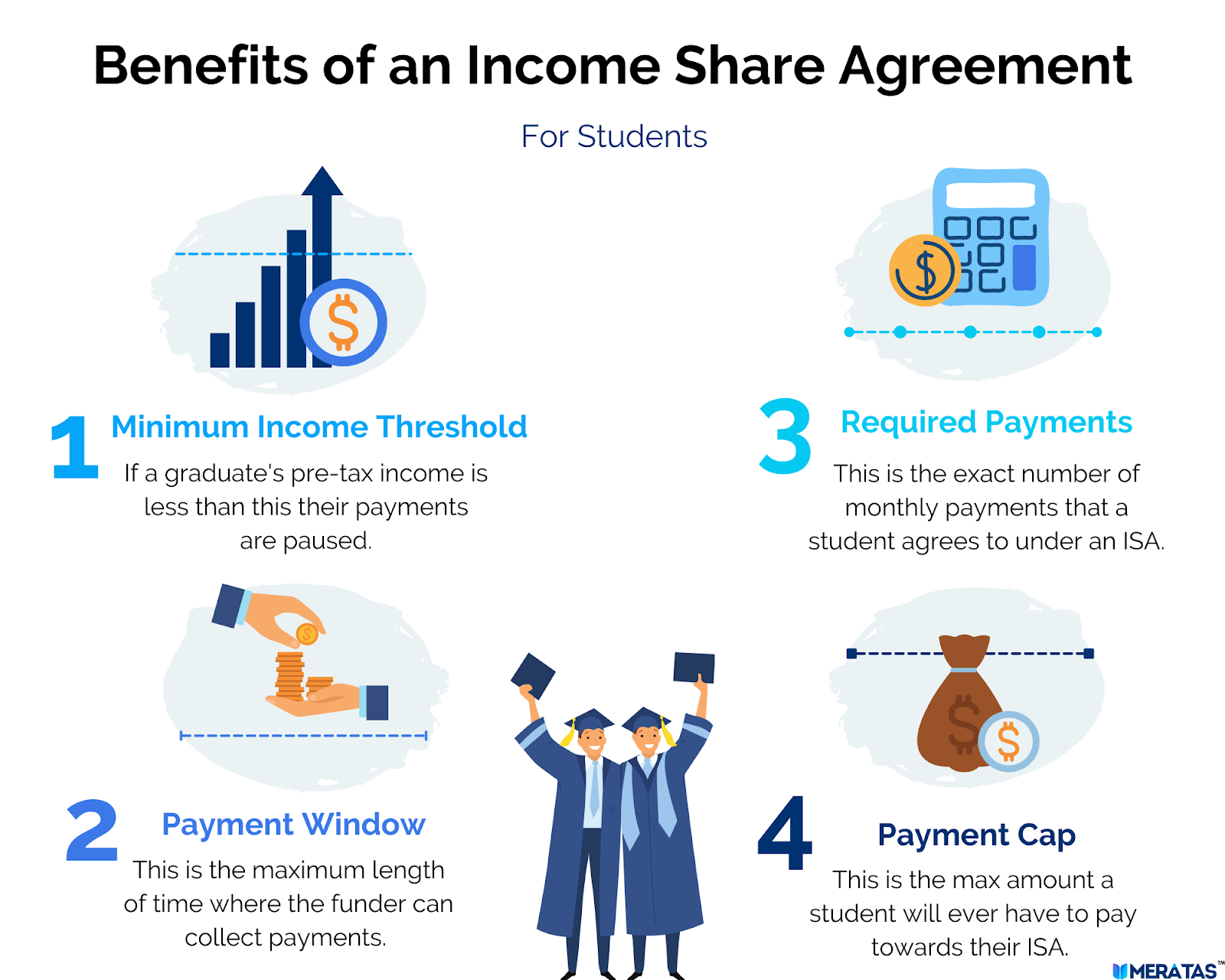

1. Make the required number of payments

With an ISA, you pay back a percentage of your earnings each month for a set number of months. Each of these payments is considered one of your Required Payments. If you pay all the Required Payments, your ISA amount is satisfied!

2. Pay the Max Payment Cap

The Max Payment Cap is built into your ISA and is the most you’ll ever need to pay towards your ISA. It is a built-in protection for high earners so that they are not punished for earning more than expected. A Payment Cap is usually some amount more than the Funded Amount (the amount the school is fronting you for their program as part of your ISA). Once your total payments reach the payment cap, your ISA is also satisfied!

3. Reaching the end of the Payment Window

The final way to end an ISA is by reaching the end of the Payment Window. The school or funder who you have an ISA with will have a set time period to collect your Required Payments or Max Payment Cap. However, if you have not reached either of those two and the Payment Window ends, you’re absolved of your ISA.

To read a more in-depth version of how to finish your ISA payments click here!

.png)

What should I be aware of before signing an Income Share Agreement?

1. Use the Income Share Percentage to calculate your future payments

Before you sign your Income Share Agreement you need to be aware of how much of your gross income you’ll end up paying each month. Remember this factor runs along a sliding scale with the Maximum Payment Cap and Payment Window. So, even if your ISA is only a small percentage, you’ll want to look at your Payment Window to determine for how long you’ll be paying that small percentage of your income to make sure it doesn’t add up to a huge total amount. Determine just how much you’ll be paying each month based on your anticipated salary, then compare that cost to traditional monthly student loan payments.

2. Double check your Payment Cap

This sum is the most you’ll ever pay towards your ISA. Traditional private loans cost the original balance, plus interest, which you’ll need to calculate to determine the true cost. With an ISA, there’s a much firmer, hard cap on payments, so it’s easier to determine total max costs. But make sure to know if your cap is a lot more than you were funded or just a little more. ISA caps tend to range from 1.2x to 2x more than you were funded. Be cautious with caps that are more than 2x what was funded to you, and avoid ISAs that don’t have a payment cap at all. Some programs utilize incremental payment caps, where the payment cap increases slowly over time. This rewards students who find early career success, by making it cheaper for them to pay off their ISA earlier in their career. Make sure to calculate what your payments might look like and determine whether the payment cap is suitable for you and your future career.

3. Understand your Payment Window

The Payment Window is how long your ISA contract lasts and is the length of time you have to pay back your required payments or Payment Cap. Think of your payment window as the total contract term. At the end of the payment window, your ISA contract expires, even if you paid back less than the amount of money you received.

To keep your ISA fair, and to prevent any potential game playing, certain situations of voluntary withdrawal from the labor force may extend your Payment Window by one month for each month of such withdrawal. For example, if you take a 6-month vacation, your payment window may pause during these break periods, and then resume when you are ready to re-enter the labor force

The most important thing to know about your Payment Window is whether your ISA lender counts months in which your payments are paused due to financial hardships towards your Payment Window or if your Payment Window is extended in those instances.

4. Double check your Minimum Income Threshold

The main benefit of an ISA is that your payments automatically pause whenever you’re unemployed or making less than the salary floor. The best part of Income Share Agreements is that during periods of deferment, there is no accruing interest like traditional student loans. The Minimum Income Threshold is how much you have to be making before you owe payments.

If your income drops below that line your payments are paused. An ISA’s salary floor should reflect your expected post-graduate income. Is your threshold lower like just $10,000? Or is it something reasonable for your career, say like $40,000. For example, Lambda School’s salary floor is $50,000 because it expects graduates to get starting salaries of at least that much. Think about what you’ll actually be able to afford, depending on where you plan on living, before you sign on the dotted line.

5. Make a note of any fines and fees

Just like with traditional student loans, there are ways to get in trouble with ISAs, if you avoid making payments. There may be some penalties for not accurately reporting your income or other scenarios with your ISA. Be sure to read and understand those possible fees and make sure you avoid any of those possible scenarios.

If you’re considering an Income Share Agreement to cover your higher education costs, then make sure to utilize an Income Share Agreement Calculator to help you figure out what your monthly payments will cost and how much you’ll pay overall.

If you think an ISA option might be right for you, make sure you take into account your ISA terms, expected future income, and calculate what your payments will look like in order to determine if an ISA is the best option for you.

What if my school doesn’t offer an ISA?

If you’re unmoved by existing Income Share Agreement providers, you could always take on the challenge of convincing your school to start its own program. That’s where Meratas comes in.

About Meratas

Meratas is the leading Income Share Agreement (ISA) software company, providing a full-service, turnkey, SaaS platform to design, originate, and manage ISAs. We help universities, bootcamps, trade schools, and membership programs increase enrollment and open accessibility to their programs. All through the power of Income Share Agreements.

We also help those looking to get an education, up-skill, or re-skill get into the career of their dreams. All at, generally, no upfront cost. We pair individuals looking for fresh new career with the best educational programs on the Meratas platforms to reach their professional goals. If you’re looking to break into your new career, check out our student page and we’ll help you find the job of your dreams.

Want more career advice, education news, and student success tips? Follow us on Twitter, LinkedIn, and Instagram!

Although every effort has been made to provide complete and accurate information, Meratas Inc. makes no warranties, express or implied, or representations as to the accuracy of content contained herein. Meratas Inc. assumes no liability or responsibility for any error or omissions in the information contained herein or the operation or use of these materials.